Hurricane Preparedness Checklist for Resilient Homes

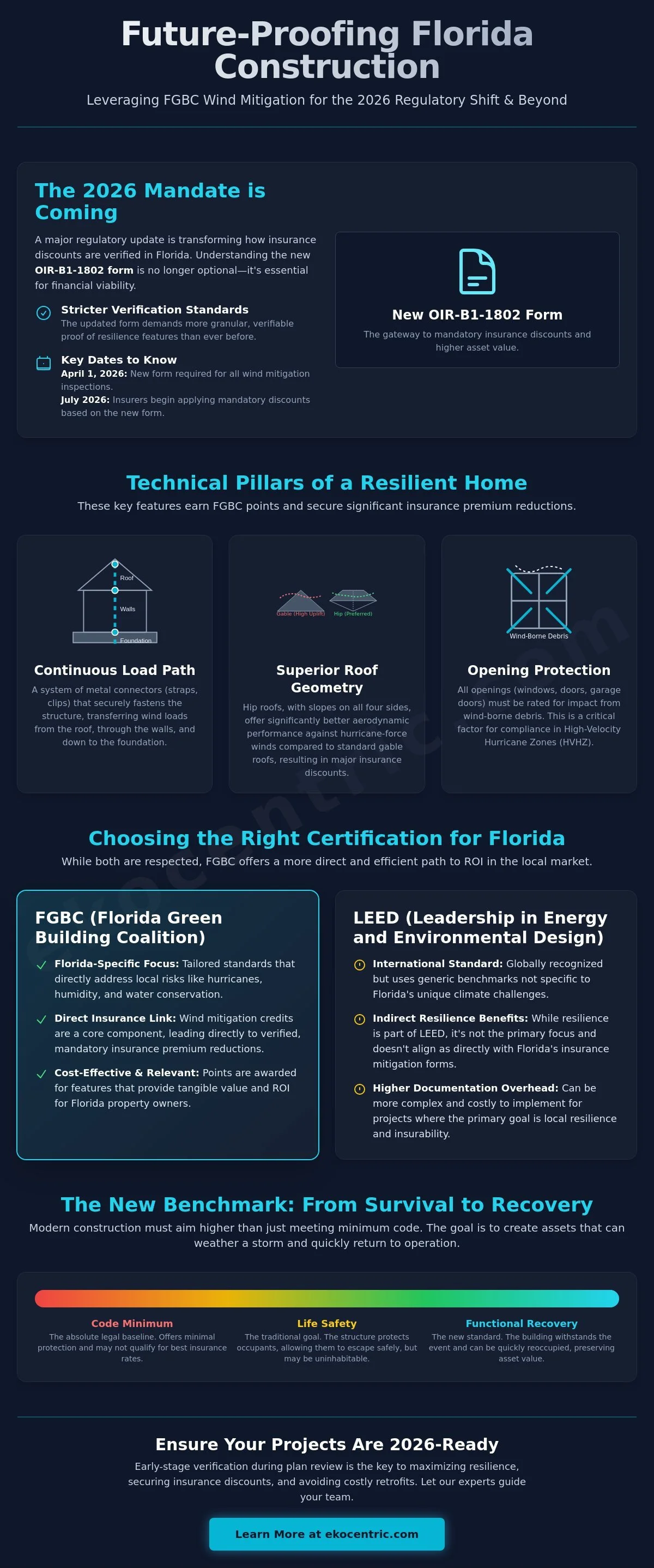

Did you know that as of April 1, 2026, every new wind mitigation inspection in Florida must utilize the overhauled OIR-B1-1802 form to qualify for mandatory insurance discounts? This regulatory shift makes understanding FGBC wind mitigation credits more than just a sustainability goal; it's a financial necessity for developers facing the strictest verification standards in over a decade. Because Florida Statute §627.0629 legally mandates these discounts, insurance companies will begin applying credits based on this new form in July 2026, leaving little room for documentation errors.

You likely feel the pressure of rising insurance premiums and the increasing complexity of High Velocity Hurricane Zone (HVHZ) compliance. It's frustrating when code requirements feel like a moving target and your team lacks the internal expertise to bridge the gap between basic code and elite certification. This guide will show you how to leverage FGBC wind mitigation credits to secure verified insurance premium reductions and achieve higher certification scores that drive real asset value. We will break down the essential components of a resilient home checklist, ensuring your projects remain competitive and protected in Florida's evolving environment.

Key Takeaways

Understand how the 2026 update to the OIR-B1-1802 form makes FGBC wind mitigation credits a vital tool for securing mandatory insurance premium reductions.

Identify the technical pillars of resilience, such as hip roof geometry and continuous load paths, that simultaneously satisfy safety codes and green building requirements.

Evaluate the strategic advantages of Florida-specific FGBC standards compared to international LEED certifications to find the most efficient path for local project ROI.

Learn why early-stage verification and consulting during the plan review phase are essential to avoid the high costs of resilience retrofitting later in construction.

Table of Contents

Understanding FGBC Wind Mitigation Credits in the 2026 Florida Market

Mapping Resilience to Green Building Certifications: LEED vs. FGBC

Understanding FGBC Wind Mitigation Credits in the 2026 Florida Market

In Florida's current insurance environment, FGBC wind mitigation credits serve as a critical bridge between structural safety and financial viability. These credits are financial incentives awarded by insurers for construction features that go beyond the baseline requirements of the Florida Building Code. While the code provides a foundation, the 2026 market demands higher standards due to increased storm frequency and the resulting volatility in insurance premiums. Carriers are no longer satisfied with minimum compliance; they're looking for verified proof of resilience.

To access these benefits, a formal windstorm mitigation inspection is required to verify that a property includes specific features like secondary water barriers or reinforced roof-to-wall connections. This verification ensures that insurers can accurately assess risk, which directly translates to lower costs for the property owner. For developers, this isn't just about saving money on a policy; it's about creating a high-performance asset that stands out in a crowded, risk-averse market.

To better understand this concept, watch this helpful video:

The 2026 Regulatory Landscape for Florida Builders

The 2026 Florida Building Code has introduced stricter requirements for wind-borne debris regions, largely driven by the adoption of ASCE 7-22 wind load standards. These updates mean that wind speed maps have shifted, and structural calculations must now account for more intense pressure cycles. Simply building to the legal minimum is no longer a guarantee of insurance eligibility in 2026. Many carriers now require documentation on the updated OIR-B1-1802 form, which demands more granular evidence of roof deck attachments and opening protections than previous versions. Projects that don't align with these standards during the design phase often face steep premium hikes or outright coverage denials. Utilizing specialized verification services early in the process ensures your project meets these evolving mandates from day one.

Wind Mitigation as a Sustainability Metric

We must move past the idea that wind mitigation is just about shutters or impact glass. True resilience is found in the fundamental integrity of the structure, from the foundation to the roof ridge. The Florida Green Building Coalition (FGBC) standard is uniquely powerful because it prioritizes local environmental risks over generic global benchmarks. While global standards are valuable, they often lack the specificity required for Florida’s unique climate. By focusing on FGBC wind mitigation credits, builders can earn points toward certification while simultaneously lowering the building's total cost of ownership. This shift moves the developer's focus from "Life Safety," which merely ensures occupants can escape, to a more ambitious goal. Functional Recovery is the new benchmark for resilient Florida assets, defining a building’s ability to maintain or quickly restore its primary operations following a major wind event.

Technical Pillars: How Wind Mitigation Earns FGBC Points

Earning FGBC wind mitigation credits requires a shift from viewing a home as a collection of parts to seeing it as a unified, resilient system. The most foundational element of this system is the continuous load path. This engineering approach ensures that wind loads are transferred from the roof down through the walls and into the foundation using specialized connectors and straps. Without this connection, even the strongest roof remains vulnerable to uplift forces. By documenting these connections during the framing stage, developers can secure higher resilience scores and meet the stringent criteria set by Florida's green building standards.

Roof geometry also plays a decisive role in a building's aerodynamic performance. Standard gable roofs create large surfaces for wind pressure to build against; hip roofs, however, distribute these forces more evenly across four sloped sides to significantly reduce the risk of structural failure. This design choice is a primary driver for insurance discounts. You can find more details on these requirements by reviewing Florida's official wind mitigation resources, which outline the specific features insurers prioritize when calculating premium credits. To ensure these technical pillars are correctly identified and documented for certification, engaging with expert verification services early in the design phase is a pragmatic step toward project success.

Structural Integrity and Wind Uplift

In High Velocity Hurricane Zones (HVHZ), securing rooftop equipment like HVAC units or solar panels is a non-negotiable certification requirement. The physics of uplift mean that 2026 standards now demand stricter roof deck attachment patterns, often requiring 8d nails spaced every six inches to resist the intense pressures defined by ASCE 7-22. While reinforced masonry remains a Florida staple, many forward-thinking developers are turning to Insulated Concrete Forms (ICF). ICF construction provides a seamless, monolithic envelope that offers superior wind resistance and energy efficiency compared to traditional hollow-core blocks. These choices don't just protect the structure; they create a high-quality living space that lasts for generations.

Opening Protection and Moisture Management

The building envelope's survival depends on its ability to withstand debris impact and prevent water intrusion. Modern impact-rated glazing has evolved to meet large missile testing standards, which simulate the impact of a nine-pound 2x4 timber at high speeds. Beyond the glass, moisture management is critical. Secondary Water Resistance (SWR), such as self-healing membranes applied directly to the roof deck, prevents internal losses even if the primary shingles or tiles are stripped away. Reinforcing the garage door is a critical step in maintaining structural integrity; its failure often leads to internal pressurization that can blow the roof off the home from the inside out. Using advanced flashing and high-performance sealants around all penetrations ensures that FGBC wind mitigation credits are backed by a truly impenetrable moisture barrier.

Mapping Resilience to Green Building Certifications: LEED vs. FGBC

Resilience and sustainability are often treated as separate operational silos, yet they are fundamentally linked by the concept of longevity. A building cannot be truly "green" if it requires total reconstruction after a major storm. By aligning structural hardening with environmental standards, developers can achieve a powerful synergy that maximizes both FGBC wind mitigation credits and high-performance certification scores. This integrated approach ensures that the resources used in construction are protected for the long term, reducing the environmental footprint associated with disaster recovery and waste.

The financial logic for this alignment is clear in the 2026 market. While certification involves specific consulting and verification fees, the resulting "Resilience ROI" is significant. According to verified 2026 data, homes with comprehensive protection can see a 20% to 30% reduction in their total annual insurance premiums. These savings, combined with the increased asset value of a third-party verified property, often offset the initial costs of certification within the first few years of operation. For a deeper look at the financial mechanisms behind these discounts, you can consult Florida's official guidance on wind mitigation, which details how state-mandated credits reward proactive hardening.

The LEED Green Rater’s Role in Wind Mitigation

In the LEED BD+C framework, hurricane resilience is increasingly recognized through "Resilient Design" pilot credits. These credits reward projects that conduct thorough vulnerability assessments and implement hardening strategies like impact-resistant envelopes and emergency power systems. A LEED Green Rater plays a vital role in this process by providing the rigorous third-party verification that insurance underwriters now demand as the "gold standard" for risk assessment. This verification ensures that the high-performance insulation and storm-hardened features described in the plans are actually present in the finished structure.

FGBC Certification: The Florida-Specific Edge

While LEED offers global prestige, the Florida Green Building Coalition (FGBC) provides a more direct and pragmatic path for local developers. The FGBC standard includes a dedicated "Disaster Mitigation" category specifically tailored to the state's unique climate challenges. Meeting these requirements often means a project automatically qualifies for the maximum FGBC wind mitigation credits available from insurers. This Florida-born standard offers a seamless transition from code compliance to elite certification. By utilizing FGBC certification consulting, project leads can navigate these requirements efficiently, ensuring that every resilience feature serves a dual purpose: protecting the asset and elevating its sustainability credentials.

The Verification Process: From Plan Review to Final Credit

Verification is often misunderstood as a final inspection, but for 2026 projects, it must begin during the plan review phase. By aligning structural engineers with sustainability experts before a single shovel hits the dirt, you ensure that FGBC wind mitigation credits are designed into the building's DNA. This proactive alignment prevents the prohibitive costs of resilience retrofitting, where builders are forced to modify existing structures to meet insurance or certification requirements. A pragmatic risk assessment at the start guarantees that every specified component, from the roof deck attachment to the window impact rating, serves the project's long-term financial health.

Integrating Resilience into the Project Lifecycle

The collaboration between structural engineers and sustainability consultants is where visionary design meets technical reality. In the 2026 market, the role of a Green Rater is indispensable for verifying that as-designed resilience actually becomes as-built reality. During mid-construction, these specialists conduct on-site inspections to verify continuous load path connections and envelope sealing before they are hidden behind finishes. For example, verified airtightness via Blower Door testing is more than an energy metric; it's a critical safeguard for post-storm moisture control. By ensuring a tight envelope, you prevent the wind-driven rain that often leads to internal mold and structural decay following a hurricane.

Documentation for Insurance and Certification ROI

Once construction is complete, the focus shifts to compiling the updated Form OIR-B1-1802 for insurance carriers. Professional documentation acts as an accelerator for the approval of wind mitigation credits, especially in complex multi-family developments where inspection failures often occur due to inconsistent record-keeping. Carriers in 2026 are increasingly selective, and a clear, third-party verified trail of evidence is the best way to secure maximum premium reductions. Partnering with a specialist for FGBC certification consulting ensures that your documentation meets both the insurer's strict criteria and the coalition's high standards. Expert-led resilience verification provides the ultimate peace of mind by confirming that your high-value assets are structurally sound and financially optimized.

Future-Proofing Florida Assets with Ekocentric Expertise

Success in Florida’s 2026 construction market requires more than just meeting code; it demands a deep commitment to environmental stewardship and structural longevity. Project leads often face a significant internal capacity gap when trying to manage multiple high-performance standards alongside complex insurance requirements. We understand that your team’s primary focus is delivery, not deciphering the nuances of evolving certification categories. This is where mission-driven expertise becomes a vital asset. By pairing visionary sustainability with pragmatic resilience, we help you transform mandatory safety measures into marketable, high-value features.

Leveraging FGBC wind mitigation credits isn't just a strategy for lowering premiums; it's a statement about the quality and endurance of your development. Properties that demonstrate this level of hardening are better positioned to weather both physical storms and economic volatility. Our approach ensures that every resilience feature is documented and verified to meet the highest industry standards. This level of precision builds confidence with investors and insurers alike, turning a compliance headache into a competitive advantage for your portfolio.

Navigating Complex Florida Standards with Ease

Managing separate consultants for LEED, FGBC, and National Green Building Standard (NGBS) verification creates unnecessary friction and fragmented data. Working with a single partner for all your green building and resilience needs streamlines the process and ensures standard alignment across the entire project lifecycle. This integrated oversight helps developers qualify for favorable financing through verified green credentials, which are increasingly required by institutional lenders. A single point of contact for verification ensures that:

Technical documentation is consistent across all certification platforms.

Site inspections are consolidated to reduce project delays.

Risk assessments are unified to satisfy both green rater and insurance underwriter requirements.

You can consult with Ekocentric to harden your next project and bridge the gap between technical requirements and financial success.

Building for the Next Generation of Florida Real Estate

The next generation of Florida real estate is defined by buildings that offer more than just aesthetics. Premium tenants and 2026 investors are prioritizing assets with verified Functional Recovery plans that guarantee a swift return to operations after a weather event. This focus on longevity and resource efficiency creates a lasting legacy of environmental responsibility. Certified resilient buildings don't just protect occupants; they maintain their marketability and asset value in a climate-conscious economy. It’s time to move beyond baseline compliance and embrace a future where your properties are built to endure. Reach out today for a comprehensive resilience and certification audit to ensure your project is ready for the challenges of tomorrow.

Securing Your Assets for Florida’s Resilient Future

Florida’s 2026 regulatory environment demands a more proactive approach to residential resilience than ever before. By shifting your focus from basic "Life Safety" to the more ambitious "Functional Recovery" standard, you protect both human life and long-term capital investment. Securing FGBC wind mitigation credits is no longer just a technical hurdle; it’s a strategic opportunity to drastically lower insurance premiums while verifying the high-performance nature of your development. Success in this landscape depends on early-stage collaboration and rigorous documentation to ensure every hardening feature is fully recognized by underwriters and certification bodies alike.

You don't have to navigate these shifting requirements alone. Partner with Florida's leading resilience consultants at Ekocentric to leverage our expert knowledge of LEED BD+C and FGBC standards. Our specialized focus on Florida's unique environmental challenges provides the precise, third-party verification that builds investor confidence and streamlines project approvals. We're dedicated to helping you turn complex code mandates into tangible business value. Let’s work together to create a more resilient and sustainable future for our state’s vibrant communities.

Frequently Asked Questions

What are FGBC wind mitigation credits and how do they differ from standard insurance discounts?

FGBC wind mitigation credits are financial incentives provided by insurers for building features that surpass the baseline Florida Building Code requirements. While standard discounts apply to basic code compliance, these credits specifically reward the advanced structural hardening required for Florida Green Building Coalition certification. This distinction is vital because it moves the property into a higher tier of verified resilience. Insurers often view these certified buildings as lower risk, which leads to more substantial and stable long-term premium reductions.

How does the 2026 Florida Building Code impact wind mitigation requirements for new construction?

The 2026 Florida Building Code incorporates the ASCE 7-22 wind load standards, which significantly increase the structural requirements for new construction in coastal regions. These updates mean that wind speed maps have been redrawn and pressure calculations are more intense. Simply meeting the legal minimum is no longer enough to secure the best insurance rates. Developers must now document specific features on the updated OIR-B1-1802 form to prove their projects can withstand these new environmental benchmarks.

Can LEED certification help my project qualify for Florida wind mitigation credits?

LEED certification can support your project's eligibility for credits, particularly through the Resilient Design pilot credits in the LEED BD+C framework. These credits align with many of the hardening strategies required by Florida insurers. However, you must still complete the state-mandated windstorm mitigation inspection. Integrating LEED rater services early in the process ensures that your sustainability goals and hurricane resilience strategies work together to satisfy both certification bodies and insurance underwriters.

What is the High Velocity Hurricane Zone (HVHZ) and where does it apply in 2026?

The High Velocity Hurricane Zone (HVHZ) consists of Miami-Dade and Broward counties, representing the areas with the most stringent wind resistance requirements in the United States. In 2026, these zones continue to set the benchmark for impact ratings and structural connections. While the HVHZ has specific legal boundaries, many developers outside these counties are choosing to build to these standards. This proactive choice often results in higher resilience scores and increased property marketability across the state.

How much can a developer save on insurance through FGBC-aligned wind mitigation?

Developers can achieve significant financial gains, with verified data from 2026 showing that comprehensive wind mitigation can reduce total annual premiums by 20% to 30%. In South Florida, where insurance costs are highest, these discounts can translate to annual savings between $800 and $1,500 per unit. These reductions represent a direct increase in net operating income. They also make the property far more attractive to long-term investors who prioritize climate-hardened assets with stable operational costs.

What is the role of a LEED Green Rater in hurricane resilience verification?

A LEED Green Rater acts as an essential third-party verifier who ensures that the resilience features specified in the design are actually implemented during construction. They conduct on-site inspections of critical components like roof-to-wall connections and building envelope sealing before they are covered by finishes. This level of verification is the gold standard for 2026 insurance companies. It provides the documented proof needed to secure maximum credits while ensuring the building meets its intended performance targets.

Is FGBC certification more beneficial than LEED for Florida-based projects?

FGBC certification is often more beneficial for projects focused purely on the Florida market because it is specifically tailored to the state’s unique climate and insurance landscape. While LEED offers international prestige, FGBC provides a more direct path to maximizing FGBC wind mitigation credits through its Disaster Mitigation category. Many local developers find it more cost-effective to achieve. It addresses regional challenges like sea-level rise and humidity more precisely than global standards that use broader environmental benchmarks.

How does the 'Functional Recovery' standard affect building costs in Florida?

The Functional Recovery standard focuses on a building's ability to remain operational after a storm, which can increase initial construction costs due to more robust structural requirements. However, this investment is offset by a dramatic reduction in long-term operational risk. Buildings designed for functional recovery avoid the massive costs of post-storm business interruption and extensive repairs. In the 2026 market, this standard is becoming the benchmark for high-value assets because it guarantees a faster return to occupancy and revenue generation.